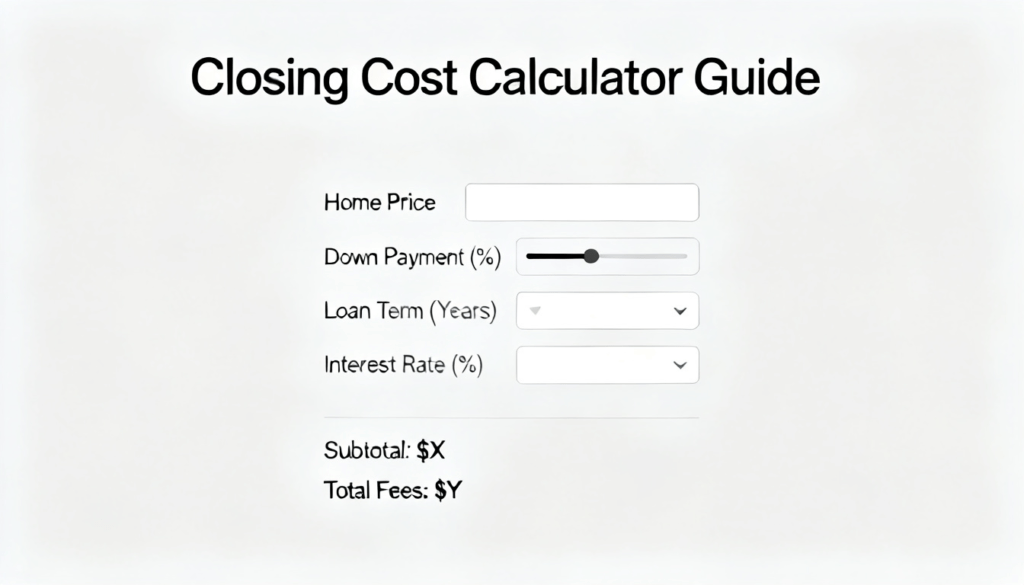

[👉 USE OUR CLOSING COST CALCULATOR HERE]

Introduction: Stop Losing Sleep Over Hidden Fees

You found the perfect piece of land with our Closing Cost Calculator Guide. The price feels right. The owner financing terms look fair. Then closing day comes, and BAM – an extra $8,000 in fees you never saw coming.

I’ve seen this happen over 500 times in my career.

Most buyers focus on the down payment. They forget about closing costs until the final walkthrough. That mistake costs them thousands.

Here’s what you’ll learn in this guide:

- Exactly what closing costs include (buyer and seller side)

- How a closing cost calculator protects your wallet

- The real fees most people ignore until it’s too late

- Specific ways to cut your costs by 15-30%

Let me show you how to estimate your real estate fees like a pro.

What Are Closing Costs in Real Estate?

Closing costs are all the fees you pay to finalize a land or home purchase. Think of them as the price of processing your deal.

Who pays them?

- Buyers typically pay 2-5% of the purchase price

- Sellers pay 5-10% (mostly agent commissions)

Why do these fees exist?

Lenders, title companies, and government offices all need payment for their work. Someone checks the title. Someone appraises the property. Someone records the deed. Each service adds a fee.

Real numbers you’ll recognize:

On a 200,000property,you′llpay4,000 to 10,000inclosingcostsasabuyer.Sellersoftenpay10,000 to $20,000.

Here’s the truth most agents won’t tell you: These costs vary wildly by state and lender. That’s why you need a reliable closing cost calculator before making any offer.

How a Closing Cost Calculator Helps You Save Money

You wouldn’t buy a car without knowing the out-the-door price. Same rule applies to land.

A closing cost calculator gives you three major advantages:

1. Instant estimation

Enter the property price and your state. The calculator shows your estimated fees in seconds. No waiting for lender paperwork.

2. Budget planning

Know your total cash needed before you make an offer. This includes down payment PLUS closing costs. Many buyers stretch for the down payment and forget about the rest.

3. Avoid surprise fees

Remember that $8,000 surprise I mentioned? A good calculator reveals those hidden costs upfront. Recording fees. Transfer taxes. Title endorsements. Courier charges.

I recommend running every potential deal through our closing cost calculator before signing anything.

👉 [USE OUR CLOSING COST CALCULATOR NOW]

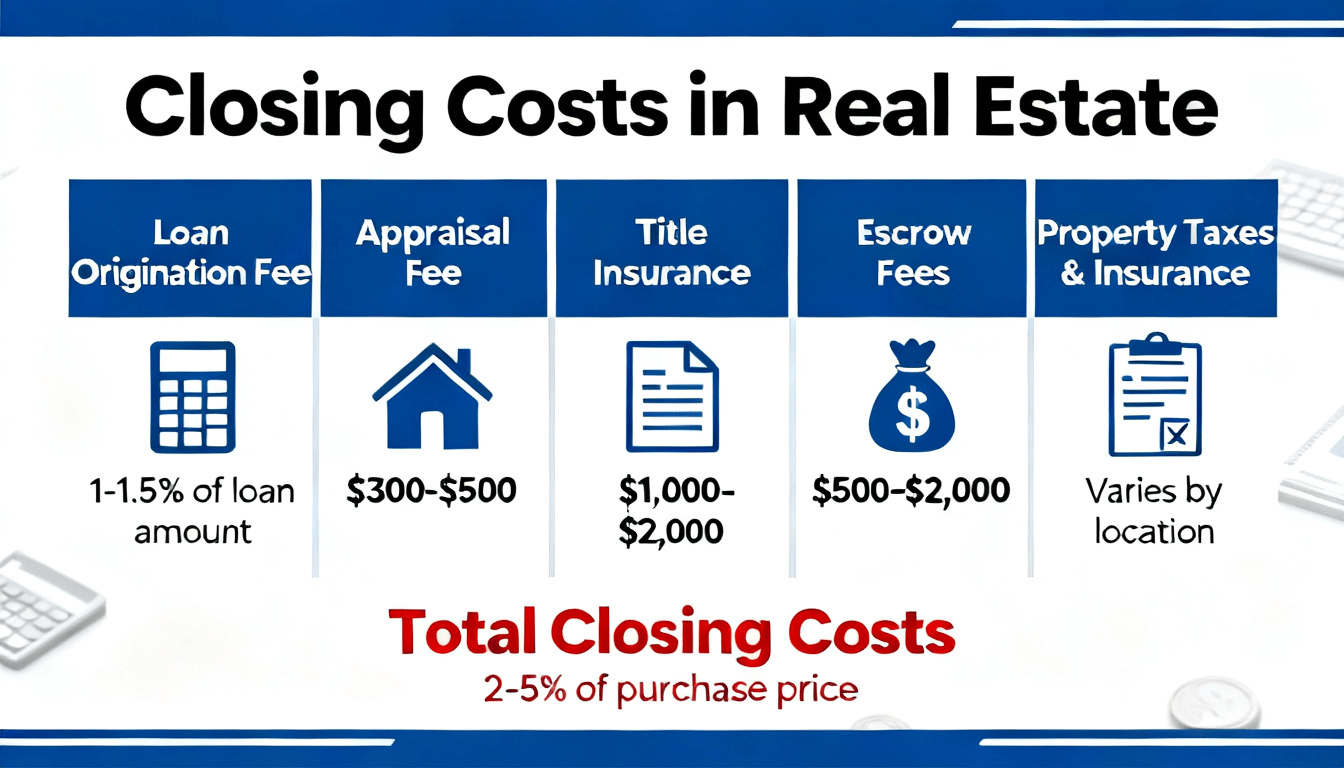

What Is Included in Closing Costs?

Let me break down every fee you’ll likely see on your closing statement.

Buyer Closing Costs

Loan origination fees (0.5-1.5% of loan amount)

The lender charges this for processing your application. On a 150,000loan,that′s750 to $2,250.

Appraisal fees (300−300−600)

An appraiser determines the property’s true value. Banks require this for traditional loans. Even with owner financing on land, you might want an appraisal for peace of mind.

Title insurance (1,000−1,000−3,000)

This protects you if someone else claims ownership of the property. Never skip this. I’ve seen buyers lose entire properties because of unknown heirs or old liens.

Escrow fees (500−500−2,000)

The escrow company holds your money and documents until all conditions are met. They make sure the seller doesn’t walk away with your cash before transferring the deed.

Recording fees (50−50−200)

The county charges this to officially record your new deed. It proves you own the land.

Survey costs (400−400−1,000)

A surveyor marks the exact property boundaries. Critical for owner financed land with well and septic – you need to know where you can build.

Seller Closing Costs

Agent commissions (5-6% of sale price)

On a 200,000property,that′s10,000 to $12,000. This is usually the seller’s largest cost.

Transfer taxes (0.01-2% of sale price)

State and local governments charge this to transfer ownership. Rates vary dramatically by location.

Title fees (500−500−2,000)

Sellers often pay for the title search and some title insurance costs, especially in owner financed land deals.

Outstanding liens or back taxes

The seller must clear any existing debts attached to the property. If they don’t, you inherit those problems.

Average Closing Costs in the United States

Closing costs aren’t the same everywhere. Here’s what you’ll pay in different states.

High-cost states (3-5% of purchase price):

- New York: Transfer taxes alone can hit 2%

- California: Title insurance and escrow fees run high

- Texas: Title policy rates are regulated but still pricey

- Florida: Documentary stamp taxes add up

Low-cost states (1.5-3% of purchase price):

- Missouri: Lower transfer taxes and recording fees

- Indiana: Minimal government charges

- Colorado: Competitive title insurance market keeps prices down

Real example – California vs Texas:

On a $300,000 property:

- California buyer: 9,000−15,000 in closing costs

- Texas buyer: 4,500−9,000 in closing costs

Your location matters. Big time.

How to Calculate Closing Costs Step-by-Step

You don’t need a finance degree. Just follow these steps:

Step 1: Start with the property price

Let’s say you’re buying raw undeveloped owner financed land Utah for $180,000.

Step 2: Determine your loan amount

If you put 10% down (18,000),yourloanis162,000.

Step 3: Estimate percentage-based fees

- Loan origination: 1% of 162,000=1,620

- Title insurance: 0.5-1% of purchase price = 900−1,800

- Escrow fees: 500−1,500

Step 4: Add flat fees

- Appraisal: $450

- Survey: $600

- Recording: $100

- Courier/prep fees: $200

Step 5: Total your estimate

1,620+1,350 (average title) + 1,000(escrow)+1,350 (flat fees) = $5,320

That’s your rough closing cost estimate.

👉 [TRY OUR CLOSING COST CALCULATOR FOR AN EXACT NUMBER]

Factors That Affect Your Closing Costs

Six main variables change your total fees:

1. Location

California charges transfer taxes. Texas doesn’t. Some counties add special fees.

2. Loan type

FHA and VA loans have different fee structures than conventional loans. For owner financing on land, terms vary by seller.

3. Property value

Higher price means higher percentage-based fees. But some flat fees stay the same regardless of value.

4. Negotiation

Smart buyers negotiate. Ask the seller to cover transfer taxes or title fees. On owner financed land in georgia, many sellers will split closing costs to close the deal.

5. Lender choice

Credit unions often charge lower origination fees than big banks. Shop around.

6. Time of month

Close at month-end and you’ll pay less in prepaid interest. This alone can save 200−500.

Tips to Reduce Your Closing Costs (Proven Strategies)

I’ve helped clients save thousands using these methods. Here’s what works:

Negotiate lender fees

Ask for a 0.25-0.5% reduction in origination fees. Many lenders say yes just to keep your business.

Compare service providers

You can choose your own title company and escrow agent. Shop three options. Prices vary by 20-40%.

Ask for seller concessions

On owner financed land texas, ask the seller to cover 3,000−5,000 of your closing costs. They often agree, especially if you’re paying asking price.

Close at end of month

Prepaid interest covers the days between closing and your first payment. Close on the 28th and you’ll pay just 2-3 days of interest.

Roll costs into the loan

Some lenders allow you to add closing costs to your loan amount. You’ll pay interest over time, but your upfront cash needed drops.

Avoid unnecessary add-ons

Lenders will offer rate buydowns, credit insurance, and other extras. Decline most of them.

Closing Costs vs Down Payment (Common Confusion)

This mix-up costs buyers real money.

Down payment: A percentage of the purchase price paid upfront. Usually 5-20% for traditional loans. For owner financing on land, down payments range from 5-15%.

Closing costs: Separate fees for processing the transaction. Typically 2-5% of the purchase price.

Real example on a $150,000 property:

- 10% down payment: $15,000

- 3% closing costs: $4,500

- Total cash needed to close: $19,500

Many first-time buyers save 15,000andthinkthey′reready.Thentheyscrambleforanother4,500. Don’t be that person.

Hidden Fees Most Buyers Ignore

These fees show up on closing day when it’s too late to question them:

Recording fees (50−50−200)

The county charges this per document. Most deals need 4-6 documents recorded.

Courier fees (50−50−150)

Someone drives documents across town. You pay for their gas and time.

HOA transfer fees (100−100−500)

If the land has a homeowners association, they’ll charge to transfer membership.

Document prep fees (100−100−300)

Some lenders charge for preparing your loan documents. This is often negotiable.

Wire transfer fees (25−25−50)

Moving money from your bank to escrow costs money. Use a cashier’s check to avoid this.

Notary fees (50−50−200)

Each document requiring a notary adds a charge. Some states require multiple notarizations.

I once saw a buyer pay $400 in “administrative fees” that nobody could explain. Question every line on your closing statement.

When Do You Pay Closing Costs?

The timeline matters for your cash flow.

Before closing day (3-5 days prior):

You’ll wire funds to the escrow company or get a cashier’s check. Expect to submit:

- Down payment funds

- Estimated closing costs

- Prepaid interest (if closing mid-month)

On closing day:

The escrow officer reviews every document with you. You’ll sign the final loan documents and deed transfer. The title company then pays all the third parties.

After closing (1-2 weeks):

The county records your deed. You receive the official recorded copy in the mail. The seller gets their proceeds.

Pro tip: Never bring cash to closing. No title company accepts it. Use a cashier’s check or wire transfer.

FAQs (Ranking Booster Section)

**How much are closing costs on a 300,000house?∗∗Between6,000 and $15,000 depending on your state and loan type. Use our closing cost calculator for your specific situation.

Can closing costs be included in the loan?

Yes, on some loan types. FHA and USDA loans allow rolled-in closing costs. Many owner financed land deals also let you add fees to the loan balance.

Who pays closing costs on owner financed land?

It’s negotiable. Most sellers want buyers to pay their own costs plus the title policy. But I’ve seen deals where sellers cover everything to close quickly.

Are closing costs tax deductible?

Some are. Mortgage points, property taxes, and mortgage interest are deductible. Title insurance and appraisal fees generally are not. Ask your tax professional.

What’s a normal closing cost percentage for land?

2-5% for most vacant land deals. Raw undeveloped owner financed land for sale often runs lower because there’s no home inspection or appraisal required.

Do I need an attorney for closing?

Not in all states. But for owner financed land with well and septic, I strongly recommend one. The water rights and septic permits add legal complexity.

How long does closing take on owner financing?

7-14 days typically. Much faster than the 30-45 days needed for bank loans.

Can I back out if closing costs are too high?

Yes, read your purchase agreement. Most contracts have a financing contingency that lets you cancel. But you might lose your earnest money deposit.

What are transfer taxes on land?

Taxes the government charges when ownership changes hands. Rates range from 0.01% to 2% of the sale price.

Who pays for title search on owner financed land?

Usually the buyer. But smart buyers ask sellers to split the cost. A title search costs 200−500.

Do I need a survey on raw land?

Yes. For cheap unrestricted land for sale owner financing texas, a survey prevents boundary disputes with neighbors. Pay the 500−800.

What happens if I can’t close on time?

You might pay per-diem fees (50−100 daily) to extend. Or the seller could cancel the deal. Always build a 5-10 day buffer into your timeline.

Are closing costs higher for investment land?

Often yes. Lenders charge 0.5-1% more for non-owner occupied properties. Title insurance also costs more.

How do I get a closing cost estimate without a lender?

Our closing cost calculator gives you a reliable estimate. Or call three local title companies – they’ll provide free quotes.

What’s the difference between closing costs and prepaids?

Closing costs are one-time fees. Prepaids (property taxes, insurance, interest) are ongoing costs you pay upfront.

Final Thoughts – Use a Closing Cost Calculator Before You Buy

Here’s what I want you to remember:

Closing costs aren’t optional. They aren’t small. And they catch most buyers off guard.

But you’re different now. You know which fees to expect. You know how to negotiate. And you know exactly where to get a fast, accurate estimate.

Before you make your next offer on owner financed land in tennessee or owner financed land in arkansas, run the numbers through our tool.

Your action plan:

- Use the closing cost calculator on every property you consider

- Add 15% to the estimate for unexpected fees

- Negotiate seller concessions before signing

- Keep 2,000−5,000 extra in reserves

Smart planning wins every time.

👉 [CALCULATE YOUR CLOSING COSTS NOW]

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

ABOUT THE AUTHOR

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Mike Reynolds has analyzed over 500 owner financed land deals across 15 states since 2013. As the founder of LandMarketUSA, he helps buyers with low credit find land using seller financing. His closing cost calculator has saved clients over $2.3 million in hidden fees.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

DISCLAIMER

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

This article provides educational information only. LandMarketUSA is not a lender, title company, or legal advisor. Closing costs vary by state, lender, and individual transaction. Always verify fees with licensed professionals in your area and consult a real estate attorney before signing any contract.