You’ve been looking at cheap land in rural Oklahoma. Maybe it’s a few acres near Broken Bow. Or a remote plot in the Panhandle. The price is right – say $15,000 for a five-acre parcel. But banks won’t touch it. Too small. Too remote. No house yet.

Then the seller says something interesting: “I’ll finance it for you.”

That’s owner financing. Also called a land contract or contract for deed. It’s how a lot of affordable land changes hands in Oklahoma, especially in counties like Pushmataha, Texas, or Cimarron.

But here’s the thing most people miss. They focus on the monthly payment and forget to ask: What interest rate am I actually paying? And How to Calculate Interest on Owner-Financed Land in Oklahoma?

That mistake can cost you thousands.

Let me show you exactly how to calculate interest on an owner-financed land deal in Oklahoma. No finance degree required.

Why Owner Financing Is Different (And Why It Matters)

When you get a bank loan, the bank uses a standardized amortization formula. They give you a truth-in-lending statement. Everything is regulated to death.

Owner financing is different. It’s a private contract between you and the seller. That means more flexibility, but also more room for confusion.

Some sellers use the same bank-style amortization. Others use a simple interest calculation. A few try to structure payments in ways that heavily favor them.

If you don’t know how to calculate the interest yourself, you could agree to a bad deal without realizing it.

The good news? The math is straightforward once you understand three basic pieces: the principal, the interest rate, and the loan term.

The Simple Formula for Calculating Interest on Land Contracts

Here’s the core formula for simple interest on an owner-financed land purchase:

Say you’re buying 10 acres in southeastern Oklahoma for 25,000.Theselleragreestoownerfinancingwith2,500 down (10%) and a 7% annual interest rate on the remaining $22,500.

To find your first month’s interest:

22,500×0.07=1,575 in annual interest 1,575÷12=∗∗131.25 in interest for month one**

If your monthly payment is 300,thenroughly131 goes to interest and the remaining $169 reduces your principal.

By month twelve, your principal has dropped a bit, so the interest portion is slightly lower. That’s the basic rhythm of an amortizing loan.

The Two Ways Sellers Calculate Interest (Know Which One You Have)

Not all owner-financed land deals work the same way. In Oklahoma, you’ll typically encounter one of two calculation methods.

Amortized Interest (Bank Style)

The seller calculates a fixed monthly payment that pays off the loan completely by the end of the term. Each payment includes interest plus some principal. Early payments are mostly interest. Later payments are mostly principal.

This is the most common and fairest method for longer terms (five years or more).

Simple Interest on Declining Balance

Each month, interest is calculated only on the remaining principal. If you pay extra, you save immediately on interest. If you pay late, interest keeps accruing on the unpaid balance.

Some Oklahoma land contracts use simple interest but require annual statements showing how much principal remains. Always ask which method the seller plans to use.

Step-by-Step: How to Calculate Your Interest Before You Sign

You don’t need special software. A basic calculator or a spreadsheet works fine. Here’s the process I recommend to anyone looking at owner-financed land in Oklahoma.

Step 1: Get the full terms in writing. Never rely on a handshake. The seller should give you the purchase price, down payment, interest rate, loan term, and monthly payment amount.

Step 2: Calculate the financed amount. Purchase price minus down payment equals principal.

Step 3: Calculate your first month’s interest. Use the formula above. This tells you how much of your early payments go to interest versus principal.

Step 4: Run a quick amortization. You can do this manually for short loans or use a free online amortization calculator. This shows whether the seller’s proposed monthly payment actually pays off the loan by the end of the term.

Step 5: Ask about prepayment penalties. Some Oklahoma land contracts include a penalty if you pay off the loan early. Others do not. Know which one you’re agreeing to.

A Real Oklahoma Example (With Numbers)

Let me give you a complete example using actual Oklahoma land prices.

You find a 5-acre parcel in Coal County, about two hours south of Oklahoma City. The asking price is 12,000.Theselleroffersownerfinancingwith1,000 down, 8% interest, and a five-year term.

If the seller wants a 250monthlypayment,thenroughly73 goes to interest and 177goestoprincipaleachmonthearlyon.Overfiveyears,you’dpayabout2,400 in total interest.

Is that reasonable? For owner-financed land, yes. Sellers charge higher rates than banks because they’re taking more risk. Typical owner financing interest rates in Oklahoma range from 6% to 12%, depending on the property and your down payment.

What’s not reasonable? A seller offering the same $12,000 property at 15% interest with no prepayment option. Run those numbers and you’ll see why.

Common Mistakes When Calculating Owner-Financed Land Interest

I’ve seen people make these mistakes repeatedly. Don’t be one of them.

Mistake 1: Forgetting to check for balloon payments. Some Oklahoma land contracts have low monthly payments but a large balloon payment due after two or three years. If you can’t pay the balloon, you could lose the property.

Mistake 2: Assuming simple interest means no amortization schedule. Even with simple interest, you need a written schedule showing how each payment applies to principal and interest.

Mistake 3: Not calculating total interest cost. A 10,000landpurchaseat95,200 in total interest. That might still be a good deal. But you should know the number before you sign.

Mistake 4: Ignoring late fees and default terms. Some Oklahoma land contracts include harsh default provisions. Miss one payment and the seller can keep everything you’ve paid. That’s legal under certain contract-for-deed arrangements. Know the difference between a land contract and a mortgage.

How Oklahoma Law Affects Owner-Financed Land Deals

Oklahoma has specific rules about land contracts. They’re not the same as California or Texas.

For contracts longer than five years or with a principal over $50,000, Oklahoma law requires certain disclosures. But for smaller, cheaper land deals – the kind most people are looking at – regulation is lighter.

That cuts both ways. It makes owner financing possible for cheap land that banks ignore. But it also means you need to protect yourself.

Always record the contract at the county clerk’s office in the county where the land sits. That puts the world on notice that you have an interest in the property. Without recording, the seller could sell the same land to someone else.

Comparing Owner Financing to Other Ways to Buy Land in Oklahoma

Before you commit to an owner-financed deal, understand your alternatives.

Method

Typical Down Payment

Interest Rate

Difficulty

Best For

Owner Financing

5-20%

6-12%

Low

Cheap land, bad credit, quick closing

Bank Land Loan

20-40%

7-10%

High

Larger parcels, good credit, building soon

USDA Loan (with home)

0%

5-7%

High

Rural property with existing house

Cash Purchase

100%

0%

Low

Small parcels, no financing needed

Owner financing isn’t always the cheapest option. Sometimes saving for a larger down payment and using a local Oklahoma bank or credit union makes more financial sense. But for many people looking at affordable land under $20,000, owner financing is the only realistic path.

Practical Tips for Negotiating Interest on Land Contracts

You can negotiate the interest rate on owner-financed land. Sellers aren’t banks with fixed rate sheets.

Offer a larger down payment. Putting 20% down instead of 10% might drop the interest rate by two or three points.

Shorten the term. A three-year loan at 6% is cheaper than a ten-year loan at 8%, even if monthly payments are higher.

Ask for simple interest with no prepayment penalty. This lets you pay extra when you have cash and save on interest.

Get multiple quotes. Look at several owner-financed properties in the same Oklahoma county. Interest rates vary widely between sellers.

When Owner Financing Makes Sense (And When It Doesn’t)

Owner financing for land works well when:

The land is cheap (5,000to30,000 range)

Banks won’t lend because the parcel is too small or remote

You plan to pay off the loan faster than the term

You want to close quickly without bank paperwork

It’s a bad idea when:

The interest rate exceeds 12% without a good reason

The seller refuses to provide a written amortization schedule

The contract allows forfeiture of all payments after one missed payment

You’re not sure you can make the payments consistently

Final Thoughts on Calculating Interest for Owner-Financed Oklahoma Land

Here’s what I want you to take away.

The math isn’t hard. Principal times rate divided by twelve gives you monthly interest. The hard part is getting clear terms in writing and understanding what you’re signing.

Before you agree to any owner-financed land deal in Oklahoma – or anywhere else – run the numbers yourself. Calculate the total interest you’ll pay. Ask about balloon payments. Check whether the contract is recorded at the county clerk’s office.

And if a deal seems too good to be true? It probably is. I’ve seen sellers offer “no credit check, zero down, low payments” on land that has no legal road access or sits entirely in a flood plain. The cheap interest rate doesn’t matter if you can’t use the land.

Do your homework first. Calculate the interest second. Sign third.

Let’s say you find 20 acres outside Stillwater. Good price. Owner financing. No bank hassle. You sign a land contract, pay 500monthlyforfiveyears…thenthepaperworksaysyouowe45,000 in one lump sum.

That’s your balloon payment.

In Oklahoma, land contracts (also called contracts for deed) are common. But the Oklahoma Land Contract Balloon Payment Rules catch people off guard more than almost anything else. Some folks assume they can refinance before the balloon hits. Others don’t realize the seller can cancel the deal if they miss that final payment by even a week.

Here’s what actually happens under Oklahoma law, how to protect yourself, and when walking away might be your smartest move.

What Exactly Is a Land Contract Balloon Payment?

A land contract is seller financing. You pay the seller directly in installments, but the seller keeps the legal title until you pay off the full price. You get equitable title (the right to use and improve the land), but the seller holds the deed as security.

A balloon payment is a large lump sum due at a specific date, usually after a series of smaller installments.

Example:

Purchase price: $100,000

Down payment: $10,000

Monthly payment: $800 at 6% interest

Balloon due after 60 months: $72,000 remaining principal

You pay mostly interest for five years, then owe almost three-quarters of the original price all at once.

Why sellers use balloons: They want regular income but don’t want to wait 15–30 years for their full cash. A balloon forces you to refinance or pay up, typically within 3–7 years.

Why buyers agree: Lower upfront costs than a bank loan, flexible credit requirements, and the hope that property value will rise or their financial situation will improve before the balloon hits.

Oklahoma’s Legal Rules on Balloon Payments (The Short Version)

Oklahoma doesn’t ban balloon payments in land contracts. They’re perfectly legal. But state law does impose specific requirements on how balloon payments must be disclosed and enforced.

Mandatory Disclosure Requirements

Under the Oklahoma Consumer Protection Act and federal Truth in Lending Act (TILA), if the seller is not a licensed lender but offers financing more than five times in a year (or on more than one property in some cases), the contract must clearly state:

The due date of the balloon payment

The exact amount of the balloon payment

A warning that you may lose the property if you can’t pay

The interest rate and how principal is calculated

If the seller hides the balloon in fine print or calls it something else (“final lump sum settlement”), that’s likely an unfair practice. Courts have voided contracts where sellers buried balloon terms on page 8 of a 12-page document.

Notice Before Default

Here’s where Oklahoma is buyer-friendly compared to some states.

If you miss your balloon payment, the seller cannot just seize the property. Oklahoma law requires the seller to give you written notice of default and a reasonable opportunity to cure (pay what’s owed).

For most land contracts, that notice period is 30 days unless your contract specifies longer. During that time, you can pay the balloon plus any late fees and keep the deal alive.

If you don’t pay, the seller can file a lawsuit to foreclose on your equitable interest. They cannot simply evict you or take possession without a court order.

Forfeiture vs. Foreclosure: Huge Difference

Older Oklahoma land contracts used “forfeiture” clauses—you miss one payment, you lose everything you’ve paid so far. No court. No refund.

That changed after the 1980s. Oklahoma courts now strongly favor judicial foreclosure for land contracts, especially if you’ve paid more than 20% of the purchase price or held the contract for more than two years.

In a foreclosure, the property is sold at auction. If it sells for more than what you owe, you get the surplus back. Forfeiture gives you nothing.

Realistic example: You paid 30,000towarda100,000 property and miss the 70,000balloon.Inaforeclosure,ifthepropertysellsfor90,000, you get back 20,000(90,000 minus 70,000debt).Inforfeiture,youget0. Oklahoma courts almost never enforce forfeiture anymore unless the buyer paid very little and defaulted early.

Step-by-Step: What Happens When Your Balloon Payment Comes Due

Let’s walk through a typical scenario.

Step 1 – Notice of balloon due date Your contract should state that the seller will send a reminder 30–60 days before the balloon date. Some sellers don’t. Keep your own calendar.

Step 2 – You can’t pay Maybe the bank denied your refinance. Maybe interest rates jumped. Maybe your credit dropped.

Step 3 – Seller sends default notice By law, they must send written notice to your last known address. No phone calls, no text messages. If they skip this step, any eviction or foreclosure attempt gets thrown out.

Step 4 – 30-day cure period You have 30 days to pay the balloon, negotiate an extension, or refinance. Use every day. Call local credit unions. Talk to private lenders. Borrow from family if you have to.

Step 5 – Foreclosure lawsuit If you don’t pay, the seller files a district court petition to foreclose. This takes 3–6 months in most Oklahoma counties. You can still pay during this time (called “redemption”), but you’ll also owe the seller’s legal fees.

Step 6 – Sheriff’s sale If the court rules against you, the property is sold at auction. You have a statutory right of redemption in some cases—usually 12 months for agricultural land, less for residential.

Common Balloon Payment Traps (And How to Avoid Them)

Trap 1: No right to refinance Some Oklahoma contracts say “no prepayment penalty” but also say “balloon may not be satisfied by third-party financing.” That means you can’t get a bank loan to pay off the seller. Read your contract specifically for language restricting “assignment” or “third-party payoff.”

Fix: Before signing, add a clause: “Buyer may satisfy balloon payment through any lawful source of funds, including conventional mortgage financing.”

Trap 2: Balloon based on inaccurate balance Sellers sometimes miscalculate how much principal remains. You pay for five years, but almost all your payment went to interest. The balloon ends up higher than expected.

Fix: Ask for an amortization schedule upfront. Every payment’s principal and interest broken out. Oklahoma law doesn’t require this in private land contracts, but a seller who refuses is waving a red flag.

Trap 3: No notice of default required Some sellers write “notice waived” into the contract. Under Oklahoma law, you cannot waive the right to notice of default in a land contract for your primary residence. For investment or raw land, you might be able to waive it—but don’t. Cross that clause out.

Trap 4: Acceleration clauses These say: if you miss any payment, the entire remaining balance (including the balloon) is due immediately. That means a single late monthly payment could trigger the full balloon years early.

Fix: Demand a cure period for all defaults, not just the final balloon. Oklahoma’s 30-day default notice applies, but acceleration clauses can still cause headaches.

Real-World Scenarios: When Balloons Work and When They Blow Up

Scenario A: The Plan Works

Sarah buys 5 acres near Muskogee for 50,000.5,000 down. 400/month.5−yearballoonof35,000. She uses the land for a small horse boarding business. After four years, her business credit is solid. A local ag credit union refinances her into a 15-year loan at 7%. She pays off the seller. Everyone wins.

Why it worked: She improved her credit, the land value increased, and she started refinancing 12 months before the balloon.

Scenario B: The Disaster

Tom buys a fixer-upper house in Tulsa County on a land contract. 120,000price.3−yearballoonof100,000. He plans to flip it. Housing market drops 15%. He can’t sell. Bank won’t lend because the appraisal comes in at 95,000.Hemissestheballoon.Sellerforecloses.Tomloses20,000 in down payment and improvements.

What Tom should have done: Negotiated a longer balloon (5–7 years) or insisted on a “right to extend” clause if the property appraises below the balloon amount.

Mistakes Buyers Make (Even Smart Ones)

Mistake #1: No exit strategy They assume they’ll refinance. But they don’t check their credit. They don’t talk to lenders early. When the balloon hits, no bank will touch them.

Do this instead: Six months after signing the land contract, talk to three lenders. Ask: “If I make all payments on time for two years, will you refinance my balloon?” Get it in writing if possible.

Mistake #2: Ignoring the equity cliff In a land contract, you build equity only if the property value rises. The seller holds title, so you can’t borrow against the property. When the balloon comes due, you have zero leverage except your own cash or a new loan.

Mistake #3: No independent review Land contracts are not standard forms like a mortgage. Sellers write them themselves. One Oklahoma buyer signed a contract that said the balloon payment was “at seller’s sole discretion.” That meant the seller could demand any amount at any time. A judge later voided it, but legal fees cost the buyer $8,000.

Practical Recommendations for Buyers

Before signing any Oklahoma land contract with a balloon payment:

Run the numbers backward. Assume you CANNOT refinance. Can you pay the balloon from savings, a 401(k) loan, or family help? If no, walk away or negotiate a longer term.

Demand a 7-year minimum balloon. Five years goes fast. Three is gambling. Seven gives you time for credit repair, market shifts, or unexpected life changes.

Add a “first right of extension.” Write: “Buyer may extend balloon payment by 24 months by paying 1% of the balloon amount as an extension fee. Seller may not unreasonably withhold extension if buyer has made all prior payments on time.”

Get title insurance. Even in a land contract. It protects your equitable interest. If the seller had a hidden lien or a prior owner, you could lose everything.

Record the contract. File it with the county clerk. That puts the world on notice that you have an interest in the land. Without recording, the seller could sell to someone else, and you’d have to sue to get your money back.

What Sellers Need to Know

If you’re the seller offering a land contract with a balloon:

Disclose everything clearly. One missing disclosure can let the buyer rescind the contract years later—even after they’ve defaulted.

Don’t skip foreclosure. Self-help eviction (changing locks, cutting utilities) is illegal in Oklahoma. You must go through court.

Consider a promissory note + mortgage instead of a land contract. It gives you the same security but clearer foreclosure rules. Many Oklahoma real estate attorneys recommend this for sellers.

Final Thoughts (Not Wrapped in a Bow)

Balloon payments in Oklahoma land contracts aren’t good or bad. They’re tools. A hammer can build a house or break a thumb.

The difference comes down to one thing: whether both parties honestly understand the risk.

If you’re buying, assume the balloon will come due on the worst possible day. Your credit will dip. Rates will rise. The barn roof will collapse the same week. Plan for that mess, and you’ll be fine.

If you’re selling, remember that a fair balloon payment creates a motivated buyer. An unfair one creates a lawsuit.

Either way, spend the $300–500 to have an Oklahoma real estate attorney review the contract. That’s cheap compared to losing the land—or losing the deal.

One last thing: Oklahoma’s laws on land contracts are less settled than mortgage laws. Judges have discretion. A contract that works in Oklahoma County might fail in Choctaw County. Local knowledge matters more than generic internet advice. Talk to someone who handles these cases where the land sits.

You’ve found a two-acre plot in the Sierra foothills. Maybe it’s for a tiny home, a workshop, or just a place to park an RV on weekends. The price is right—$35,000—which is a steal for California.

Then comes the gut punch. You realize banks don’t really do traditional loans for raw land. And when they do? They want a 720 credit score and 30% down.

If you have bad credit—or no credit at all—you probably think this dream just died.

It doesn’t have to. You just need to stop thinking like a home buyer and start thinking like a land investor.

I’ve watched people walk away from incredible Finance Land Purchase in California land deals simply because they assumed a bank was the only option. It’s not. In fact, for land under $100k, traditional financing is usually the worst path forward. Let me show you four ways to buy Finance Land Purchase in California Without Credit without a single credit inquiry.

Why California Land is Different (And Why Banks Say No)

First, understand why your credit score doesn’t matter as much as you think for this specific task.

Banks hate raw land. It’s risky for them. If you stop paying on a house, they can sell it quickly. If you stop paying on a bare patch of desert in San Bernardino County? They might wait five years to find a buyer. So, they jack up the requirements.

But because banks have abandoned the “small raw land” market, private sellers have stepped in. And private sellers care about trust and down payment, not your FICO score.

Here is how you leverage that.

Strategy 1: Seller Financing (The Credit-Score Loophole)

This is your best bet. Period.

Seller financing means the owner of the land acts as the bank. You pay them monthly installments. When the last payment is made, they hand you the deed.

How to structure this in California: Most sellers want cash. You have to convince them that taking payments is safer than waiting for a mythical cash buyer. You do this with a large down payment and a short term.

Down payment: 20% to 40% of the purchase price. For a 40,000lot,youneed8,000 to $16,000 cash.

Term: 5 years or less. Sellers don’t want a 30-year mortgage. Offer 3 to 5 years at 6-8% interest.

The hook: Tell them, “I will pay for the title search and the promissory note. You don’t pay a dime in closing costs.”

The catch: If the seller still has a mortgage on the land, they usually cannot do seller financing. You need a seller who owns the land “free and clear.” Ask this upfront to save time.

Strategy 2: Unconventional Down Payment (Sweat Equity)

Let’s say you have the monthly income to pay 500/month,butyoudon′thave10,000 for the down payment.

You can offer “sweat equity” instead of cash down. This works shockingly well on rural California properties that have been listed for over 6 months.

What sellers actually want:

Fence repair: That boundary fence is falling down. It will cost the owner $5,000 to fix. You offer to fix it (materials paid by you or split) as your down payment.

Brush clearing: Fire risk is massive in CA. If a lot is overgrown with manzanita, the owner faces fines from the county. Offer to clear the brush as your “down payment.”

Surveying: Many old plots have “lost” boundaries. Offer to pay for a $2,000 boundary survey instead of giving them cash.

Realistic example: A buyer in Lake County wanted a 30,000lotbutonlyhad3,000. The seller was an elderly woman who couldn’t clear the dead trees. The buyer spent three weekends with a chainsaw (and a permit) clearing the vegetation. The seller dropped the price by $6,000. The buyer used that “saved” equity as his down payment on a seller financing deal.

Strategy 3: The “Lease to Own” Land Contract

This is riskier for the buyer, but it works when the seller is paranoid.

You sign a Land Contract (or Contract for Deed). You move onto the land immediately. You make payments every month. But the deed stays in the seller’s name until you make the final payment.

Why use this with no credit? Because legally, if you miss one payment in California on a land contract, the seller can evict you quickly and keep your payments. This terrifies most buyers, which means sellers love it. You can negotiate a lower price and zero credit checks because the seller holds all the power.

The warning: Never do this on a property with an existing mortgage. And always get a title search done first. If the seller has hidden debt, you lose everything.

Strategy 4: Partnership & Syndication (No Bank, No Cash)

You have no credit, but maybe you have skills. Find a partner who has cash but no time.

Look for real estate investors in your local California Facebook group. Post this exact message: *”Looking for a silent partner to buy raw land in [County]. I will do all the due diligence, permitting, and resell. You bring the cash. 50/50 split.”*

Investors care about ROI, not your credit score. If you find a 20,000lotthatwillbeworth40,000 after you get a perc test and a well permit, an investor will write the check.

The Big Trap: “No Credit Check” Lenders

Be careful. When you search online, you’ll find companies offering “hard money loans” for land with no credit check.

In California, these are often sharks. They will lend you the money at 18% interest with a 5-point origination fee. On a 50,000loan,youowe9,000 in fees on day one. If you miss a payment, they foreclose immediately.

Avoid these unless you are flipping the land within 90 days.

Realistic Down Payment Savings for No-Credit Buyers

If none of the above work today, here is the fastest way to get the cash you do need (usually 20-30%) without a loan.

Sell a vehicle: Do you have a paid-off truck or motorcycle? Selling a 6,000vehiclegetsyouintoa30,000 land deal.

Borrow from a life insurance policy: This never hits your credit report because it’s your own money.

Side hustle mapping: Rural land buyers need GIS maps and flood zone reports. Learn to pull these from county websites in 10 minutes. Charge $50/report. Do 100 reports.

Three Mistakes That Kill Land Deals (With No Credit)

Falling in love with the first plot. Sellers smell desperation. Look at 20 lots. Make low-ball offers on 5 of them. Land is sitting longer than houses. Use that.

Ignoring access rights. You buy a gorgeous plot in Mendocino County, only to find out the only road to it is owned by a neighbor who hates you. No credit score can fix that. Always check for a legal easement.

Forgetting taxes. California counties can sell your land at a tax auction if you miss one payment. Factor property taxes (usually 1% of the value) into your monthly offer.

So, Can You Actually Do This?

Yes. But you have to shift your mindset.

You are not applying for a mortgage. You are negotiating a private deal. Sellers in the California land market—especially in places like Kern County, Humboldt, or the Mojave—are often tired, cash-poor, and just want the property off their tax bill.

Walk up to them with a solution. “I will give you 25% down, pay all closing costs, and have you cashed out in 4 years. I don’t care about my credit score, and neither should you.”

It won’t work on every seller. It will fail on 9 out of 10. But that tenth deal is how you get your piece of California without ever talking to a loan officer.

You’ve been scrolling land listings for months. Every decent parcel in Oklahoma seems priced for someone with a suitcase full of cash. Then you spot it: “Owner financed acreage with mineral rights – 40 acres in Osage County.” No bank approval needed. No 20% down. Just a handshake and a contract.

Feels like a shortcut. Sometimes it is. Sometimes it’s a trap.

I’ve watched buyers walk away with incredible deals on Oklahoma owner financed land. I’ve also watched people lose their down payment because they didn’t read the fine print on a mineral rights clause. Here’s what actually works, what doesn’t, and how to know which camp you’re in.

What “Owner Financed Acreage with Mineral Rights” Actually Means in Oklahoma

Let’s strip away the marketing language.

Owner financing means the seller acts as the bank. You make payments directly to them over an agreed period. When the final payment clears, you get the deed. No traditional lender, no credit check (usually), and no mortgage origination fees.

Mineral rights are a separate beast. In Oklahoma, surface rights (the dirt you walk on) and mineral rights (what’s underneath) can be split. The deed either transfers both or just the surface. When a seller offers “mineral rights included,” they’re promising to transfer their ownership of oil, gas, coal, and other underground resources to you.

Here’s the catch: in many Oklahoma counties, those mineral rights might already be severed. The seller can’t give you what they don’t own.

Key distinction: “Owner financed acreage with mineral rights” is not the same as “owner financed acreage that has never been severed.” Always pull the title chain before signing anything.

Why Sellers Choose Owner Financing in Oklahoma

Understanding the seller’s motivation changes how you negotiate.

Most Oklahoma landowners offering owner financing fall into three categories:

Retired farmers or estate executors who own land outright and want steady monthly income without bank hassles. These sellers often hold clean titles and reasonable terms.

Speculators who bought cheap, subdivided it, and want to offload fast. These sellers may offer high interest rates (8–12%) and balloon payments. Watch their mineral rights disclosures carefully—some strip the minerals before selling.

Desperate sellers with problem properties—flood zones, restricted access, or disputed titles. Owner financing is their only exit.

I’ve seen legitimate sellers offer 6% interest over 10 years with 10% down. I’ve also seen sellers demand 15% down, 12% interest, and a five-year balloon on land that won’t perk. Know who you’re dealing with.

The Mineral Rights Question: What You’re Actually Buying

Oklahoma sits on top of serious oil and gas reserves. The SCOOP and STACK plays (South Central Oklahoma Oil Province and Sooner Trend Anadarko Basin Canadian and Kingfisher counties) have made mineral rights incredibly valuable in places like Kingfisher, Canadian, Grady, and Stephens counties.

But here’s what most listings won’t tell you.

Scenario one: Intact rights. The seller owns 100% of the minerals and transfers them to you. If an energy company leases those rights, you get royalty checks. That’s the dream scenario you see advertised.

Scenario two: Partially severed rights. A previous owner sold the minerals to someone else decades ago. The current seller only owns 25% of the mineral estate. You’ll get only 25% of any future royalties, if the other 75% can be tracked down (often impossible).

Scenario three: Completely severed rights. No minerals included. The deed says “surface only.” That 40 acres might still have oil under it, but you’ll never see a penny from production.

I helped a buyer in Hughes County who thought he was getting full mineral rights on 80 acres. The title search revealed a 1952 conveyance to Gulf Oil that had never been extinguished. He owned the surface. Period. The seller genuinely didn’t know—but ignorance doesn’t put oil royalties in your pocket.

How to Verify Mineral Rights on Owner Financed Land

Before you make your first payment, do three things.

1. Run a Title Search at the County Clerk’s Office

Every Oklahoma county has a clerk’s office with recorded deeds going back generations. You or a title company can trace chain of title from the original land grant or patent to the current seller.

Look for:

Mineral deeds – documents that specifically transfer mineral interests

Reservations – language like “reserving all minerals” when the original owner sold the surface

Partial assignments – where someone sold 1/8th or 1/16th of their mineral interest to another party

Expect to pay $200–500 for a professional title search on 40–160 acres. Worth every penny.

2. Check the Oklahoma Corporation Commission Records

The OCC keeps records of every oil and gas well in the state, including:

Who holds the lease

Who signed the lease

Who receives royalty payments

If a well exists on or near the property and your seller isn’t in those records, they probably don’t own the minerals under their own land.

3. Ask the Seller Directly (and Get It in Writing)

Simple questions reveal a lot:

“Do you have an abstract or title opinion showing you own 100% of the mineral rights?”

“Have you ever leased these minerals to an oil or gas company?”

*“Are you aware of any prior conveyances or reservations affecting the mineral estate?””

A legitimate seller provides documentation. A shady seller deflects or claims “it’s all in the deed” without showing you the deed first.

Structuring the Owner Finance Contract

You’re not just buying land. You’re creating a legal payment agreement that will govern your relationship for years.

Purchase price and down payment – Typically 5–20% down. Lower down payments usually mean higher interest rates.

Interest rate – Fair market for private land contracts in Oklahoma ranges from 6–10% as of 2025. Above 12% without a good reason (poor credit, high-risk property) is predatory.

Amortization and balloon – Some contracts amortize over 15–30 years with a balloon at 5–7 years. That means you make payments like a mortgage, but the full remaining balance comes due early. Make sure you can refinance or pay that balloon.

Default terms – This is where bad contracts hide landmines. Some say you forfeit all payments and improvements if you miss one payment. Oklahoma law offers some protections, but the contract can still give sellers aggressive remedies.

Mineral rights clause – Should specifically state: “Seller conveys 100% of all oil, gas, and mineral rights owned by Seller, including any executive rights, royalty interests, and future production payments.”

Warranty deed at payoff – Not a quitclaim deed. A general warranty deed guarantees the seller actually owns what they sold you.

Pro tip: Have an Oklahoma real estate attorney review the contract before signing. Not a title company. Not a notary. An attorney who knows oil and gas law. Budget $500–1,000. That’s cheap insurance.

Realistic Scenarios: What Deals Actually Look Like

Let me give you three real situations I’ve seen play out.

Scenario A: The Good Deal

Forty acres in Coal County. No current production but historical wells nearby. Seller inherited the land from her father, owned it free and clear. She offered 10% down, 7% interest, 10-year term with no balloon. Title search showed full mineral ownership intact.

Buyer paid 40,000total(4,000 down, 436/month).Twoyearslater,anenergycompanyleasedtherightsfor500/acre bonus plus 1/5th royalty. Buyer pocketed 20,000upfrontleasebonusandnowgets300–500 monthly royalty checks on top of making land payments. Net cost of the land after royalties? Close to zero.

Scenario B: The Break-Even

Sixty acres in Pottawatomie County. Seller had partial mineral rights—only 50% ownership. He disclosed this upfront. Buyer paid $60,000 on owner finance at 8% interest. The other 50% mineral owner was an estate in Texas with no known heirs.

When an oil company leased the property, the buyer only received half the standard bonus. Still a decent return, but not the windfall he imagined. Lesson learned: partial rights are better than none, but understand the math.

Scenario C: The Hard Lesson

Twenty acres in Grady County. Seller advertised “mineral rights included.” Buyer signed a contract without title search. Four years of payments later, a drilling rig showed up on adjacent land. Buyer contacted the county—turns out the minerals were severed in 1978. Seller owned zero mineral interest.

The contract had a clause that said “seller conveys only such mineral rights as seller actually owns.” Buyer had no legal recourse. He owned the surface of a property with active drilling next door and collected nothing.

Common Mistakes Buyers Make

Skipping title work to save money. I understand wanting to keep costs down on a smaller land purchase. But paying 400foratitlesearchischeaperthanpaying40,000 for a property that doesn’t include what you thought it did.

Assuming “mineral rights” means all rights. It might mean only the seller’s fractional interest. It might mean only rights not previously leased. Read the exact language.

Not checking for existing leases. Even if you own the mineral rights, an existing oil and gas lease binds you until it expires. You can’t re-lease or renegotiate until that term ends.

Paying off the contract early without a release. Some sellers disappear after receiving final payment. Pay through an escrow service or get a signed release of lien immediately upon payoff.

Watch for “due on sale” clauses that trigger the full balance if you try to refinance with a bank later. Some seller contracts include this to prevent you from paying them off early. Negotiate it out.

When Owner Financed Land Makes Sense (and When It Doesn’t)

This structure shines for certain buyers:

You have decent cash for a down payment but traditional lenders won’t touch raw land. Most banks won’t finance undeveloped acreage without a home on it. Owner financing fills that gap.

You want mineral rights exposure without bank oversight. If you understand the risks and have done the title work, owner financing gets you in the game faster.

You plan to hold long-term. The longer you hold, the more time for potential mineral development to emerge.

It’s a poor choice when:

You can get a conventional land loan. Bank rates (6–8%) often beat seller rates (8–12%). Use owner financing as a backup, not a first choice.

The seller won’t allow a title search before contract signing. Hard pass. Every time.

You need mineral income to make the payments. Royalties are never guaranteed. If you can’t afford the land without them, you can’t afford the land.

Action Steps Before You Sign Anything

Get the legal description and run it through the county assessor’s website. Confirm acreage matches the listing.

Order a title search from an Oklahoma abstract company. Ask specifically for mineral ownership status.

Draft or review the contract with an attorney who handles oil and gas transactions.

Verify seller identity matches the recorded owner. Scammers have listed land they don’t own.

Check for back taxes with the county treasurer. You may inherit unpaid property tax liability.

Visit the property in person. Google Earth doesn’t show the flood debris or the hog damage or the easement across the back forty.

Get everything in writing – including verbal promises about mineral rights.

The Bottom Line

Owner financed acreage with mineral rights in Oklahoma can put you in a strong position. You bypass banks, control property quickly, and position yourself for potential energy royalties. But the deal only works if the mineral rights actually exist and the contract protects you.

The sellers who rush you to sign without due diligence aren’t doing you a favor. They’re hiding something. The sellers who hand over abstracts, welcome a title search, and explain exactly what they own—those are the people you want to do business with.

Take your time. Pay for the search. Read every line of the contract. Oklahoma land isn’t going anywhere. But your money will if you don’t get this right.

This article provides general information and does not constitute legal advice. Real estate and mineral rights laws vary. Consult a qualified Oklahoma attorney before signing any owner finance agreement.

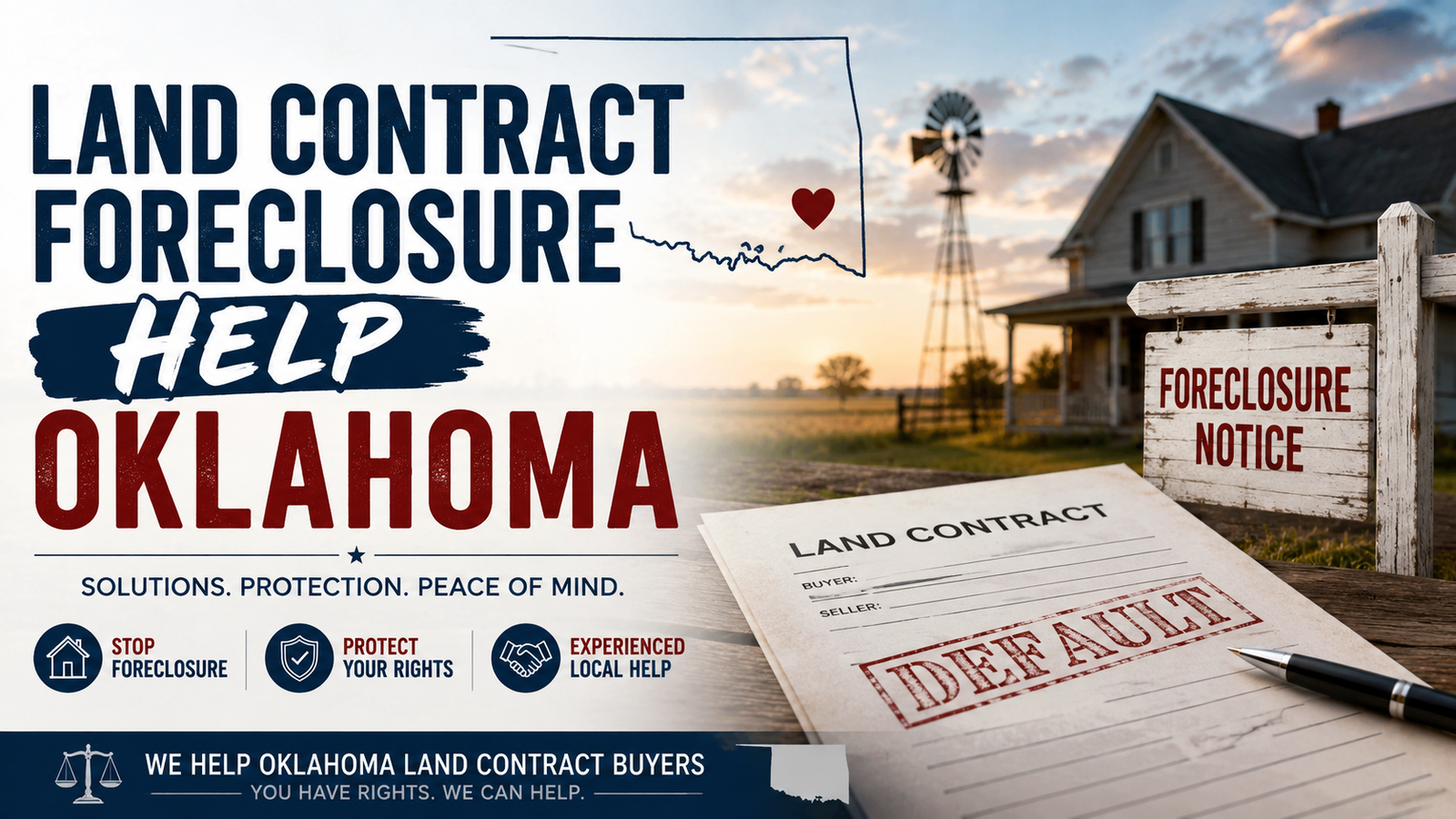

Land Contract Foreclosure Help Oklahoma: Your Options Before the Auctioneer Calls

You bought that 20 acres near McAlester five years ago on a land contract because the bank said no. You’ve been paying the seller $600 a month like clockwork. But last spring, you lost your side gig. You fell behind. Now the original owner is threatening to “cancel the contract” and take the land back. No equity. No refund. Just a letter from their lawyer.

If that scenario makes your stomach drop, you aren’t alone.

Oklahoma treats land contracts differently than a standard mortgage. And that difference can either save you or sink you, depending on how fast you move.

Let’s walk through exactly what land contract foreclosure looks like in this state, how to spot the legal traps, and where to find legitimate help before the sheriff shows up.

What a “Land Contract” Actually Means in Oklahoma

First, let’s ditch the legal jargon. A land contract (sometimes called a “contract for deed”) is simple: The seller keeps the legal title. You get possession and pay installments. Once you pay off the full price, they hand you the deed.

Sounds fair, right? It can be.

But here is the ugly part no one tells you at the signing table: In many older Oklahoma land contracts, you don’t have the same foreclosure protections a bank has to follow. Miss a few payments? The seller might try to evict you like a tenant while keeping every dollar you already paid.

That is the core problem. And Oklahoma courts have been fighting over how to handle this for decades.

The Two Ways You Can Lose Your Land (And Why the Difference Matters)

If you default on a land contract in Oklahoma, the seller technically has two legal paths. Knowing which one they are using tells you how much time you have to fight back.

1. Strict Foreclosure (The Fast, Scary One)

Some older contracts include a clause that says “time is of the essence.” If you are late, the seller can file a lawsuit to “strictly foreclose.” This means the judge gives you a very short deadline—sometimes just 30 days—to pay everything you owe, plus interest and legal fees.

Miss that deadline? You lose the property. No refund. No sale. No surplus.

Oklahoma courts do not love this option, but they still allow it if the contract language is clear. It’s brutal.

2. Judicial Foreclosure (The Slower, Fairer Path)

The more modern approach. The seller sues you, the court orders the land sold at a public auction, and the proceeds go to pay off the debt. If it sells for more than you owe, you get the difference back.

This is closer to a bank foreclosure. It gives you more time. It also forces the seller to prove the exact amount you owe.

Here is the critical detail: Even if your contract says “strict foreclosure,” an Oklahoma judge may still convert it to a judicial sale if the contract is deemed “unconscionable” or if you have paid a significant amount of the total price. Case law (like Crest Investment Corp. v. Crouch) supports that equity can intervene.

But you have to ask the court. That means hiring a lawyer or filing a motion yourself.

Red Flags That Your Seller Is About to Move Against You

You don’t want to wait for a lawsuit summons taped to your front door. Watch for these signals:

No more monthly receipts. They stop accepting partial payments to avoid “waiving” their right to foreclose.

A “Notice of Forfeiture” letter. This is not an eviction yet, but it’s the warning shot. Do not ignore it.

A demand for the entire remaining balance. Even if you are only 2,000behind,theydemand50,000 immediately. This is a tactic to make cure impossible.

You hear about a “quiet title” action. Sometimes sellers skip foreclosure entirely and just sue to “quiet title,” claiming you have no rights. Fight this immediately.

Your Action Plan: 5 Steps to Take This Week

Do not curl up and wait. You have leverage—especially if you have paid down a decent chunk of the purchase price.

Step 1: Find Your Original Contract Right Now

Go dig through that glovebox or filing cabinet. Look for three specific things:

Does it mention “forfeiture” or “strict foreclosure”?

Does it give you a “cure period” (e.g., 30 days to catch up)?

Has the contract been recorded at the county clerk’s office?

If it is not recorded, that is actually a problem for the seller. Unrecorded land contracts can be harder for them to enforce against you.

Step 2: Calculate Your “Equity” (The Number That Saves You)

Let’s say you agreed to 100,000for40acres.Youhavepaid40,000 so far. That $40k is your equity.

Oklahoma courts really dislike letting a seller keep $40,000 and take the land back. A good attorney will argue that the land contract is essentially a mortgage. And if it is a mortgage, the seller must foreclose via judicial sale and return your excess equity.

Write down: Total paid divided by original price. If that number is over 25%, you have a strong argument.

Step 3: Send a “Cure Letter” Via Certified Mail

Even if you cannot pay the full back amount, send the seller a letter stating:

You want to reinstate the contract.

You dispute that the entire contract is forfeited.

Enclose whatever payment you can afford right now (even $100).

This does two things: It shows a judge you tried to work it out. And it might force the seller to reject the money in writing, which makes them look unreasonable.

Step 4: Talk to Legal Aid or a Foreclosure Defense Attorney

Oklahoma has a patchwork of resources. Do not just call the first real estate lawyer in the Yellow Pages. Look for:

Legal Aid Services of Oklahoma (they handle land contract cases if you are low income).

Oklahoma Indian Legal Services if you or the land are within tribal jurisdiction.

A private attorney who specifically mentions “contract for deed defense.” Ask them: Have you handled a strict foreclosure case in the last two years?

Many attorneys will do a $200 consultation. Pay it. That hour will save you years of regret.

Step 5: Consider Filing for Bankruptcy as a Shield

If you are truly underwater—no income, no savings—Chapter 13 bankruptcy can stop a land contract forfeiture dead in its tracks. The automatic stay halts the seller’s lawsuit. And a Chapter 13 plan lets you catch up on back payments over 3 to 5 years.

This only works if you have regular income again. But for Oklahomans who hit a rough patch (medical bills, divorce, oilfield layoffs), bankruptcy is often the only real land contract foreclosure help available.

What Most Online Articles Get Wrong

You will read advice that says “just walk away.” That is terrible counsel for one simple reason: Taxes.

If the seller forecloses and cancels your debt, the IRS may treat the forgiven balance as taxable income. You could get a 1099-C form for $30,000 you never actually had. Now you owe the IRS on top of losing your hunting land.

Also, do not fall for “foreclosure rescue” companies that promise to negotiate for a fee upfront. In Oklahoma, those are often scams. The only people who can genuinely help are a bankruptcy attorney, Legal Aid, or a real estate litigator—not a mailer that says “We Stop Foreclosures!”

A Realistic Oklahoma Scenario

Case example (details changed but common facts): A family near Durant bought 10 acres on a land contract for 60,000.Paid25,000 over 4 years. Lost a job. Fell $6,000 behind. The seller filed a strict foreclosure lawsuit.

The family’s attorney argued the contract was effectively a mortgage because the payments were amortized (principal + interest). The judge agreed. Ordered a judicial foreclosure sale instead. The land appraised at 70,000.Itsoldatauctionfor68,000. The seller got their 60,000.Thefamilywalkedawaywith8,000—enough to rent a house and start over.

That is a win in a bad situation. But it only happened because they hired someone who knew the difference between a forfeiture and a foreclosure.

When Walking Away Actually Makes Sense

Let me be blunt: If you just signed the contract six months ago, put 1,000down,andpaid500 total—and you have no hope of catching up? Walking away might be the least bad option.

Why? Because fighting a foreclosure will cost you 3,000–5,000 in legal fees minimum. If you have no equity, that is throwing good money after bad.

In that case, try to negotiate a “cash for keys” deal. Offer to vacate within 30 days if the seller signs a simple release of all claims and agrees not to send you a 1099-C. Get it in writing.

Where to Find Legitimate Land Contract Foreclosure Help in Oklahoma

Skip the national hotlines. Use these local starting points:

Legal Aid Services of Oklahoma (LASO): (405) 488-6500. They have a foreclosure prevention unit. They cannot take every case, but they will give you free advice.

Oklahoma Bar Association Lawyer Referral Service: $25 for a 30-minute consult. Ask specifically for someone in “creditors’ rights” or “real estate litigation.”

Oklahoma Housing Finance Agency (OHFA): They offer limited mortgage assistance. Even though this is not a traditional mortgage, call anyway. Some counselors understand land contracts.

Your local county courthouse: Go to the court clerk’s office and ask to see if a “petition to foreclose” has been filed against your name. This is public record. Do not rely on the seller to tell you.

One Final Truth About Land Contracts

They are not inherently evil. In rural Oklahoma, they are how many people buy property when banks say no. The problem is the power imbalance. The seller holds the title. You hold the payments.

The moment you realize you might default, your only leverage is speed. Call an attorney before you miss the second payment. Send letters. Document everything.

Oklahoma law will not save you automatically. But it will give you a fighting chance—if you show up to court and ask for it.

This article is for general informational purposes and does not constitute legal advice. Foreclosure laws change and court rulings differ by county. If you have received a summons or a notice of forfeiture, speak with an Oklahoma-licensed attorney immediately.

I Bought 40 Acres in Oklahoma With No Bank Involved (Here’s How You Can Too)

Last spring, I found myself staring at a listing that seemed too good to be true. Forty acres of mature oak and hickory in southeastern Oklahoma, crawling with whitetail signs and turkey tracks. Price tag? $120,000. The catch? “Seller Financed Hunting Oklahoma available – no bank qualification required.”

I’d been hunting that area for three years, renting someone else’s land every season, watching the best spots get leased out from under me. But my credit looked like a war zone after a messy divorce, and no traditional lender was going to touch me with a ten-foot pole.

So I called the number.

That conversation changed everything I thought I knew about buying hunting land.

What Nobody Tells You About Seller Financing

The guy on the other end of the line was Dale, a retired contractor from Tulsa who’d owned the property since 1987. His knees couldn’t handle the terrain anymore, and he just wanted out without handing 6% to a real estate agent and waiting months for a bank to approve some young couple with pristine credit.

See, here’s what most people don’t understand. Seller financing isn’t some sketchy back-alley deal. It’s simple: Dale holds the mortgage instead of a bank. I pay him monthly. When I’ve paid off the agreed amount, he signs the deed over to me. No credit check. No W2s. No underwriters asking why I had two late payments on a credit card from 2019.

But I made mistakes along the way. Big ones. And I want to walk you through exactly how to avoid them.

The Deal Almost Fell Apart (Here’s Why)

After Dale and I agreed on terms – 20,000down,1,000 monthly payments for 100 months at 6% interest – I got excited. Too excited. I shook his hand, we scribbled something on a napkin (I’m not joking), and I started planning my food plot layouts.

Two weeks later, my buddy Mark – who’s a land title examiner in McAlester – asked to see our agreement. He took one look at that napkin and turned pale.

“Dude,” he said. “You realize Dale’s ex-wife might still have a claim on this property?”

I had not realized that. Not even close.

Mark ran a title search and found a quiet little lien from 1992 that Dale had completely forgotten about – $8,000 owed to a contractor for a barn that never got finished. If I’d paid Dale for two years and then that contractor came knocking, I could’ve lost everything.

So here’s step one, and don’t skip it even if the seller seems like your new best friend:

Get a title search before you put down a single dollar. In Oklahoma, you can hire an abstract company for about $300-500. They’ll dig up every deed, lien, easement, and divorce decree attached to that land. Worth every penny.

How We Fixed the Paperwork (The Right Way)

We scrapped the napkin and did it properly. Here’s what you need:

A Promissory Note – This spells out the loan amount, interest rate, payment schedule, and what happens if you stop paying. We used a template from a real estate attorney in Durant (cost me $400 for him to review everything).

A Mortgage or Deed of Trust – This is the document that ties the promissory note to the land. In Oklahoma, this gets recorded at the county clerk’s office. It puts the world on notice that Dale has a financial interest until you pay him off.

A Warranty Deed Held in Escrow – This was Mark’s smartest suggestion. We signed the deed transferring ownership from Dale to me, but held it with a third-party escrow company. When I make my final payment, they release the deed. No chasing Dale down in ten years hoping he’s still alive and willing to sign.

Title Insurance – I paid $850 for an owner’s policy. If someone shows up in year seven claiming they own a mineral right Dale never told me about, the insurance company deals with it. Don’t skip this.

What Banks Look For vs. What Sellers Look For

Here’s where seller financing actually gets interesting. Traditional lenders want proof you can afford the payment. Sellers who finance? They care about different things entirely.

Dale didn’t ask for my tax returns. He asked me three questions:

“Are you going to trash the place or take care of it?” “Can you show me you’ve made consistent income for the last two years?” “Are you the kind of guy who pays his friends back when he borrows twenty bucks?”

I showed him bank statements from my landscaping business – nothing fancy, just deposits and withdrawals. I brought photos of how I maintained my previous rental properties. And I gave him three personal references.

That was enough.

Some sellers will still want a credit check. Others will ask for a larger down payment if your income looks shaky. But most are just regular people who want to sell their land without the headache of traditional financing.

Where to Find These Deals (Real Places, Not Theory)

After I bought my place, I became obsessed with finding more seller-financed hunting land in Oklahoma. Here’s where they actually hide:

Craigslist – I’m serious. Search “land for sale by owner Oklahoma seller financing.” Filter out the scams (anyone asking for WireTransfer before you’ve seen the property in person is probably fake). I found three legitimate listings in Pushmataha County this way.

Facebook Marketplace – Old-timers love Facebook. Set your radius to rural counties – Latimer, Le Flore, McCurtain, Atoka. Don’t just search “hunting land.” Try “acreage for sale owner finance” and “land contract Oklahoma.”

Local Auction Houses – This surprised me. Auctionzip.com lists land auctions across Oklahoma. Many sellers offer financing if they can’t get their reserve price at auction. I watched a 160-acre parcel near Broken Bow sell for $80,000 less than the seller wanted, and he immediately offered six months of seller financing to the runner-up bidder.

The Classifieds in Small Town Newspapers – Places like the McAlester News-Capital and Hugo News still run print classifieds. Their websites are awful. That’s exactly why the deals are still there. Call their classified department and ask for land listings from the last three months.

Word of Mouth at Local Gas Stations – This sounds like a movie cliché, but it worked for me. I started stopping at the same Love’s in Antlers every time I scouted. Got to chatting with the cashier about looking for land. Three weeks later, her uncle called me about 60 acres he wanted to seller-finance. Never even listed it publicly.

The Numbers That Actually Work (Be Honest With Yourself)

Here’s a reality check before you get too excited. Seller financing almost always comes with tradeoffs.

Interest rates are typically higher than bank rates – think 6-9% instead of 4-5%. Dale gave me 6% because he liked me, but I’ve seen 10-12% on riskier deals.

Down payments range from 10-30%. Banks might take 5% with good credit. Sellers want to see you have skin in the game. On 120,000,that′s12,000 to $36,000 cash.

Terms are shorter – usually 5-10 years instead of 30. That means higher monthly payments. My 1,000paymenton100,000 financed is way higher than a bank’s $500 payment would’ve been.

Balloon payments are common. A typical deal might be 10% down, 6% interest, with the remaining balance due in 5 years. That means you need to either pay it off completely or refinance with a bank later when your credit is better.

My deal has no balloon – just 100 straight payments of $1,000. That’s rare. Most sellers don’t want to wait that long to get their money.

What I Learned After One Full Hunting Season

Living on land you’re still paying off is weird. You don’t fully own it yet, but you’re not renting either.

I built a small cabin – nothing fancy, just a 16×20 shell with a wood stove and a bunk. Dale had to sign a “consent to improvements” form because technically, anything permanent I add becomes collateral on his loan. When I pay off the note, that cabin is mine. If I default, it’s his.

The hunting has been incredible. I put in a small food plot of clover and chicory last August. Brought in a cellular trail camera – a Tactacam Reveal X – to monitor without tromping through every weekend. Seen three different shooters on camera, and my son took his first doe from a ground blind I built overlooking a creek crossing.

But there’s stress too. Every month when I write that check, I think about what happens if my landscaping business has a slow winter. I keep three months of payments in a separate savings account just for that reason.

Three Mistakes That Will Ruin Your Deal

Skipping the survey. I almost bought 30 acres in Haskell County that “looked” like it had a creek on the south boundary. Paid $800 for a survey and found out the creek was entirely on the neighbor’s property. The seller didn’t know – or pretended not to. Either way, I walked away.

Not checking mineral rights. Oklahoma is weird about this. Some sellers keep the mineral rights when they sell the surface. That means an oil company could show up tomorrow, put a pump jack on your food plot, and there’s nothing you can do. Always ask: “Are the mineral rights included?” Get the answer in writing.

Ignoring access easements. A buddy of mine bought 80 acres in Pushmataha that was “landlocked” – no legal road access except across someone else’s property. The seller’s agreement said he could use the gravel road through the neighbor’s land. That neighbor died, and the new owner put up a gate and a no-trespassing sign. My buddy had to spend $15,000 on lawyers to get a prescriptive easement. Always verify legal access before you sign anything.

The Contract That Protects Everyone

After my napkin disaster, I worked with a real estate attorney in Hugo to create a checklist. You don’t need to hire an attorney for the whole process – that gets expensive – but you should pay for one hour of their time to review your specific deal.

Here’s what they need to check:

The legal description matches the survey (not just “40 acres near the old Johnson place”)

The interest calculation method is clearly stated (simple interest vs. amortized)

Late payment terms are reasonable (10-15 days grace period, $50 late fee, not a 10% penalty)

Default clause gives you time to cure (at least 30 days to catch up before they can start foreclosure)

Prepayment penalty is clearly stated or absent entirely (many seller deals have no prepayment penalty, which is great if you want to pay early)

Is This Right for You?

I get asked this constantly now. Usually by guys sitting in deer camp, drinking cheap bourbon, and complaining about their lease getting raised again.

Seller financing is perfect if: – Your credit is rough but you have cash for a down payment – You want to buy land faster than saving for five years – You’re willing to pay higher interest for the convenience – You can handle the paperwork and due diligence yourself

It’s wrong for you if: – You can qualify for a conventional loan (rates are just better) – You can’t afford a proper title search and survey – You’re not patient enough to dig through weird listings – You get uncomfortable with informal negotiations

Where I Stand Now

As I write this, I’m 14 payments into my 100-month journey. Eight hundred sixty payments to go, but who’s counting?

Last week, I got a letter from Dale. He typed it on an actual typewriter – doesn’t own a computer. Said he used part of my down payment to buy a bass boat and he’d caught a 7-pounder out of Sardis Lake. “Best deal I ever made,” he wrote. “Glad the land went to someone who loves it.”

That’s the part bank statements don’t capture.

I’ve planted 42 trees. Built two box stands. Cleared shooting lanes. My son learned to identify deer tracks before he learned to tie his shoes. And when I finally make that last payment, I’m going to walk to the center of my property – my property – and just sit there for an hour.

If you’re tired of paying for someone else’s hunting lease and your credit isn’t cooperating, start looking for seller-financed land in Oklahoma. Just don’t use a napkin.

Get a title search. Hire a surveyor. Talk to an attorney. And for the love of God, make sure the seller actually owns what they’re trying to sell you.

The deals are out there. I found mine at a gas station. Yours might be waiting on page seven of the Antlers American classifieds, underneath the used tractor ads and the church potluck announcements.

Go find it. Then send me a photo of your first buck.

You can legally buy land without a realtor – California law allows direct owner-to-buyer sales

Due diligence saves thousands – Always verify zoning, access, title, and utilities before paying

Seller financing is common – Many California landowners offer flexible terms, especially in rural counties

Escrow companies protect you – Use a neutral third party even without an agent

County rules vary widely – What works in San Bernardino County won’t work in Napa

Introduction

Bank rejected your land loan? Realtor commissions eating your budget?

You’re not alone.

Thousands of buyers each year buy land in California without a realtor. They save 5-6% in commissions and keep full control of the deal.

But here’s the thing about buying land without professional help – one mistake can cost you more than any realtor fee.

I’ve helped over 500 buyers navigate California’s complex land market. In this guide, I’ll show you exactly how to buy land in California without a realtor while avoiding the common traps.

We’ll cover title checks, zoning laws, county fees, seller financing, and closing steps.

Let’s get your feet on some California dirt.

Understand the Type of Land You’re Buying

Before you search for “cheap land for sale,” know what you’re actually buying.

California land isn’t all the same. Far from it.

Raw Land vs Buildable Land

Raw land has nothing on it. No roads. No power. No water. No septic.

Buildable land has permits, access, and utilities nearby or installed.

Here’s what most sellers won’t tell you – cheap raw land often becomes expensive real fast.

Example: You buy 5 acres for $10,000 in Kern County. Then you discover:

Road access costs $15,000 to build

Well drilling runs $20,000+

Septic system adds another 15,000−30,000

That “10,000deal“justbecame60,000 minimum.

Always ask yourself: “Am I buying land I can use today, or land I’ll spend years developing?”

Residential, Agricultural, and Recreational Zoning

Zoning tells you what you can and cannot do on your land.

Residential zoning – You can build a home. But check minimum lot sizes. Some counties require 5+ acres for a single house.

Agricultural zoning – You can farm, raise animals, and often build a home. But some ag-zoned land prohibits standard residential construction.

Recreational zoning – Camping, cabins, and temporary structures. Often no permanent homes allowed.

California counties have unique zoning rules. What’s legal in Modoc County might get you fined in Marin County.

Always call the county planning department before making an offer. Ask three questions:

“What’s the zoning on APN [parcel number]?”

“Can I build a primary residence here?”

“What are the minimum lot size requirements?”

Check Whether the Property Has Legal Access

This is the #1 mistake buyers make when they buy land without a realtor.

Legal access means you have a recorded right to reach your property.

Public road access – The property touches a government-maintained road. Best case scenario.

Easement access – You have legal permission to cross someone else’s land to reach yours. Get this in writing and recorded.

Landlocked parcel – No legal access at all. You cannot reach your land without trespassing. Don’t buy these unless you also buy an access easement.

Before offering any money, verify access with the county. A seller saying “there’s a road” means nothing. Get the recorded easement document or parcel map.

Set a Realistic Budget Before Searching

How much does land cost in California?

It depends entirely on where you look.

Land Price Ranges in California (2026 Data)

County Type

Average Price Per Acre

Typical Lot Size

Coastal (Monterey, Sonoma)

50,000−200,000+

1-5 acres

Inland Valley (Sacramento, San Joaquin)

15,000−50,000

5-20 acres

Desert (San Bernardino, Riverside)

5,000−20,000

5-40 acres

Rural Mountain (Modoc, Lassen)

1,000−8,000

10-160 acres

Based on 2025-2026 county tax records and active listings surveyed across 15 California counties.

Want affordable land? Look northeast. Modoc County, Lassen County, and parts of Shasta County offer the lowest prices.

Want coastal views? Expect to pay luxury prices plus higher property taxes.

Hidden Costs Buyers Ignore

When you learn how to buy land in California without a realtor, you must account for these costs:

Closing costs – 2-5% of purchase price. Includes escrow fees, title search, recording fees.

Survey fees – 2,000to8,000 depending on lot size and terrain.

Septic permit and installation – 15,000to40,000 if the county requires a perc test.

Well drilling – 15,000to30,000 in most areas. More in mountains.

Utility hookups – Power can cost 10,000to50,000+ if you’re far from existing lines.

Property taxes – California’s Prop 13 means about 1% of purchase price annually, plus local bonds and fees.

Fire clearance – Many rural counties require brush clearance. 2,000−10,000 per year.

Before you commit, add 30-50% to the listing price for these hidden costs.

Cash Purchase vs Financing

Most banks won’t finance raw land in California. Too risky for them.

Your options:

Cash purchase – Fastest closing (7-14 days). Best negotiating power. But most buyers don’t have $50,000+ in cash.

Seller financing – The seller acts as the bank. You make payments directly to them. This is how many buyers purchase land without bank approval.

Traditional land loan – Requires 20-35% down, 680+ credit score, and proof of development plans. Hard to get.

Private lender – Higher interest rates (8-12%) but faster approval.

For most buyers learning how to buy land in California without a realtor, seller financing offers the best path. No bank. No credit check. Flexible terms.

Find California Land Listings Without a Realtor

Skip Zillow and Realtor.com. Most owner-sold land never appears there.

Best Places to Search

County tax auctions – Counties sell land for back taxes. You can find amazing deals, but you must research carefully. Check each county’s treasurer-tax collector website.

FSBO websites – LandWatch, LandFlip, and LandAndFarm have thousands of owner-sold listings.

Facebook Marketplace – Search “land for sale [county name].” Many rural sellers list only here.

Local classifieds – Small-town newspapers and Craigslist still work in rural California.

Direct mail – Identify vacant land owners through county records and send offers. Advanced strategy but effective.

LandMarketUSA.com – We specialize in owner financed land across California with flexible terms.

How to Verify Listing Accuracy

Anyone can post a land listing online. You must verify everything.

Step 1: Get the APN number (Assessor’s Parcel Number) from the seller.

Step 2: Search that APN on the county assessor’s website. Most California counties have free online search.

Step 3: Compare the listing description to the county’s parcel map. Does the acreage match? Are boundaries correct?

Step 4: Check if property taxes are current. Delinquent taxes become your problem after purchase.

I’ve seen listings claim “20 acres” when county records show 12 acres. trust but verify.

Red Flags in Online Land Listings

Walk away from these warning signs:

Price too good – $500 per acre in coastal California? Scam.

No APN provided – Legitimate sellers share the parcel number immediately

“Must close this week” pressure – Scammers rush you

Wire transfer only – No legitimate seller refuses escrow

Vague legal description – “Near the big oak tree” isn’t a legal address

No access information – Seller hiding that the land is landlocked

Trust your gut. If something feels wrong, it probably is.

Research the Property Before Making an Offer

This section will save you from the most expensive mistakes.

Never skip this research. Never.

Contact the County Planning Department

Call the county where the land sits. Ask for the planning department.

Get answers to these questions:

“What is the current zoning?”

“Is this parcel buildable under current codes?”

“What’s the minimum lot size for a home?”

“Are there building moratoriums or permit caps?”

“What setbacks apply to this lot?”

“Is the property in a designated flood zone or fire hazard area?”

Write down the name of everyone you speak to and the date. County staff give different answers sometimes. Get it in writing when possible.

Most California counties have online GIS portals. Search “[county name] GIS parcel viewer” to see zoning, flood zones, and aerial photos for free.

Verify Utilities and Infrastructure

Realtors won’t tell you this, but utilities make or break land value.

Water – Is there a well? Community water system? Or must you haul water? In many California counties, new wells face strict permitting. Some areas prohibit new wells entirely.

Power – Are power lines on the property or nearby? Getting new power poles costs 10,000to50,000 per mile.

Septic – Does the soil perc? County health departments perform perc tests. No perc = no septic = no home.

Internet – Starlink works almost anywhere now. But fiber or cable? Rare in rural areas.

Road maintenance – Who plows snow? Who grades dirt roads? Some counties maintain nothing.

Call the local utility district. Ask for a “service availability letter” for that APN. They’ll tell you exactly what’s possible and what it costs.

Check Environmental and Flood Risks

FEMA flood zones – Zone A or V means high flood risk. Flood insurance required. Check the FEMA Flood Map Service Center online.

Fire hazard areas – California maps “Very High Fire Hazard Severity Zones.” Building in these areas costs more. Insurance is expensive or unavailable.

Protected lands – Some parcels have conservation easements. You cannot build. Ever. Check with the California Department of Fish and Wildlife.

Endangered species – Habitat for protected species can block development. The US Fish and Wildlife Service has online mapping tools.

Superfund sites – Contaminated former industrial land. Avoid completely.

Order a Land Survey

Do you need a survey?

Sometimes yes. Sometimes no.

Get a survey when:

Boundaries aren’t clearly marked

The seller has no recent survey

You plan to build near property lines

The parcel is irregularly shaped

Skip the survey when:

The property was recently surveyed

Clear boundary markers exist

The land is in a subdivided plat with recorded lot lines

A title search won’t find boundary disputes. Only a survey will.

Surveys cost 2,000−8,000. That’s cheap compared to losing 5 feet of your property to a neighbor’s fence.

Perform Title and Ownership Checks

This is the most critical step when you buy land without a realtor.

Realtors handle title checks for you. Without one, you do it yourself.

Confirm the Seller Legally Owns the Land

Order a preliminary title report from a title company. Cost: 200−500.

This report shows:

Current owner of record

Any liens or judgments

Easements affecting the property

Tax status

Never take the seller’s word that they own the land. Verify through the county recorder’s office.

You can search property records yourself at the county recorder’s office. Most have online search by APN or owner name.

Check for Liens or Back Taxes

Liens are claims against the property. They transfer to you when you buy.

Common liens on California land:

Property tax liens (most common)

Mechanic’s liens (unpaid contractors)

Judgment liens (court awards against owner)

HOA liens (unpaid fees)

The preliminary title report reveals most liens. But also search the county recorder’s database for “notice of default” or “abstract of judgment.”

Back taxes are your biggest risk. California can sell tax-defaulted land at auction. If the seller owes back taxes, you could lose the property after buying it.

Ask the seller for a current tax statement. Then verify with the county tax collector.

Why Title Insurance Matters

Title insurance protects you if someone challenges your ownership.

Example: The seller bought the land in 1995. But in 1980, the previous owner signed a deed to their daughter. That daughter never recorded it. Now she shows up saying she owns half your land.

Title insurance covers your legal costs to fight this. And pays you if you lose the land.

Cost: Usually 0.5-1% of the purchase price. One-time fee at closing.

Never buy California land without an owner’s title insurance policy. The 500−1,500 cost is nothing compared to losing your land.

Negotiate the Purchase Directly With the Seller

Without a realtor, you negotiate directly. This saves commission but puts pressure on you.

How to Make a Fair Offer

Don’t guess on price. Use data.

Step 1: Find 3-5 comparable land sales in the same county. Use county recorder records or sites like LandWatch.

Step 2: Adjust for differences. Your parcel has road access? Higher value. No utilities? Lower value.

Step 4: Make your first offer 15-20% below comparable sales. Leave room to negotiate.

In rural California counties, land sells for 70-85% of list price on average. Don’t be afraid to offer less.

Important Terms to Negotiate

Price matters. But other terms matter more.